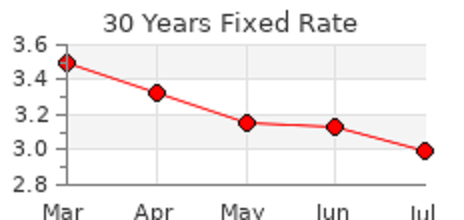

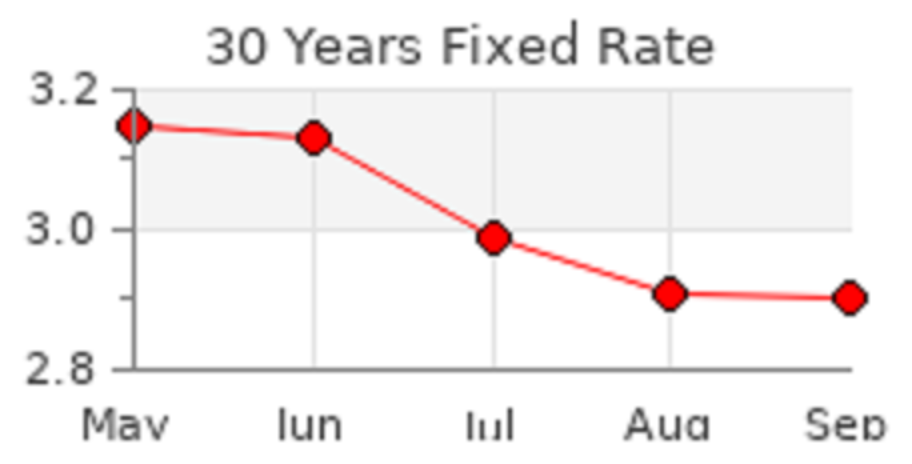

30 Year Mortgage Rates pushed lower last week reaching a new low of 2.88%, according to Freddie Mac, a government-sponsored agency that backs millions of American mortgages. Congressional gridlock over the next fiscal relief could drive rates even lower.

The limited supply of homes on the market continue to cause an obstacle to buyers looking to own a home. Credit tightening is also putting a squeeze on buyers to qualify for these record low rates.

Message me if your thinking about buying a Fort Collins or Loveland home at m.me/EdPowersRealEstate

Ed Powers Real Estate 970-690-3113 ed@EdPowersRealEstate.com www.EdPowersRealEstate.com

When Congress passed Section 4021 of the CARES Act in response to the effects of COVID-19, their intent was to help borrowers who were having problems making their mortgage payments. Little did Congress realize that they were potentially setting up borrowers for trouble in the future when it comes to credit worthiness as assessed by the lending community.

According to Mark Hanf, president of Pacific Private Money, “Section 4021 of the CARES Act contained a regulation that loan servicers “shall report the credit obligation or account for those participating in forbearance as current”. In other words, those participating in a forbearance program should not see their credit scores drop. However, there is a loophole that allows lenders to discover whether or not a borrower is actually making payments. It is the “comments” section of a credit report. The CARES Act does not mention the comments section of credit reports, and that’s where forbearance notations are going.” What borrowers are not being told is that any reference in a credit report to forbearance can be a Scarlet Letter for an applicant seeking a new mortgage, according to Kathleen Howley in an article she wrote in early May 2020.

According to Hanf, within a week of Howley’s article, his company received a loan request from a home buyer who was denied credit from a major bank for just this very situation. Although the bank sees the existing mortgage as “current” the forbearance has let the world know via the comment section that this borrower has requested a deferment. The major bank involved would most likely not deny the loan on its face due to the deferment, as this would violate the law; however, banks are notorious for coming up with a myriad of reasons for denying a loan and still stay within the guidelines set out for them.

Conventional lenders desire to have plain vanilla borrowers who pay back loans in a timely manner. When a borrower changes terms of the loan by requesting principal forgiveness or other aspects of the

loan, the lenders generally do not usually extend credit again to these borrowers and can negatively affect the borrower’s ability to borrow again from unrelated lenders. Such is the case back during the Great Recession wherein some borrowers took advantage of the economic climate by asking their lender to reduce the principal of their loan [total forgiveness rather than just a deferment]. The borrowers may have gotten a reprieve, but the long-term effects may have been more drastic. Similarly, to when a borrower files bankruptcy. The borrower may get out of paying creditors, but their ability to borrow in the future is usually severely hampered.

In one case, back in 2009, during the heart of the Greta Recession, one banker tells a story of how a wealthy borrower first asked for a principal loan reduction of $500,000 because his collateralized real estate had decreased and his request was granted. But, when this borrower was faced with the prospects of having this reduction reported on his credit report or the fact that he would have to inform any new lender that he requested a principal reduction [as this question is usually on bank applications], he voluntarily requested that the $500,000 abatement be reinstated. He decided his ability to borrow in the future was worth more than the $500,000 principal reduction.

Borrowers will have to decide if requesting deferments is worth the risk of potential future lending restrictions based upon the lender desire to lend to borrowers who choose to defer mortgage payments when the opportunity arises. Whoever said, “there’s no free lunch” must have been talking about these very situations.

Message me if your thinking about buying or selling a Fort Collins or Loveland home at m.me/EdPowersRealEstate

Ed Powers Real Estate 970-690-3113 ed@EdPowersRealEstate.com www.EdPowersRealEstate.com

Scoffers label it, ‘panic-moving.’ Others call it common sense. Wherever you stand, there is little doubt that, as the pandemic continues to surge, the flight of families from city to suburbs is picking up steam across the nation. “Young New York couples typically put off a move to the suburbs until after the birth of their second child,” said Elizabeth Nunan, president of Houlihan Lawrence, a leading New York residential brokerage. “It gives them time to save some money and enjoy the perks of city living until the need for space and the cost of childcare make the family-friendly suburbs a better choice.” But circumstances

have flipped the concept on its ear. “Living in the epicenter of the coronavirus pandemic left most New Yorkers justifiably fearful,” Nunan said. CONTINUED >>>

Despite the ongoing coronavirus pandemic, the real estate market must go on. Homeowners still need to sell, house-hunters still need to buy, and real estate agents still need to make a living. But the typical home selling process involves frequent contact with strangers—which is not recommended during this time of social distancing. By now, you’re probably getting pretty good at making adjustments in your everyday life to protect the health and safety of yourself and those around you. Along the same lines, there are steps you can take to show your home to potential buyers without risking your health or hurting your chances of a sale. Here are some tips to prepare your home for sale in the coronavirus CONTINUED >>>

For many first-time buyers, a Federal Housing Administration (FHA) loan is the prudent—and often the only—choice for a mortgage. With the flexible credit and low down payment requirements, an FHA loan makes it easier to qualify than almost any loan out there. However, the ongoing private mortgage insurance (PMI) you have to pay when you have an FHA loan makes your monthly payments more expensive. And, unlike a conventional loan, which allows you to remove your PMI at a certain point, you can never get rid of it with an FHA loan—even when you have tons of equity in your home. So, with rates at historic lows, should you refi out of your FHA loan to a conventional loan? We’re looking at the pros and cons. Pro: You can get rid of private mortgage insurance (PMI) “FHA loans require certain provisions which sometimes place a heavy burden on a homeowner’s budget, often in the form of premiums paid for mortgage insurance,” said PennyMac. That mortgage insurance on an FHA loan ranges from .45–1.05% of your home loan amount every year. On a CONTINUED >>>

Read about the events shaping the Real Estate market today, find current interest rates, or browse the extensive library of advice and how-to articles written by some of the top experts in Real Estate. Updated each weekday.

Ever wonder how mortgage lenders set interest rates for their loan programs each and every business day? Wonder why some lenders quote the exact same rate for the exact same program? Maybe why one lender is lower than others? Here’s some insight on how mortgage lenders set their rates each day.

First, note that mortgage lenders set their rates on the same basic set of indices. There are some exceptions, primarily mortgage lenders who issue their own loan programs that intend to keep the loans internally and collect interest on the loan rather than selling the note.

Adjustable rate mortgages and fixed rate mortgages are priced a bit differently. An adjustable rate mortgage, or ARM, is tied to a specific, universally tradeable index, such as the 1-Year Constant Maturity Treasury. Each morning, the “secondary” departments of these mortgage companies look up the current price of an ARM index and then add a margin to it. If for example the index came in at 1.75% and the margin was set at 2.00%, the new rate for that specific program would come in at 3.75% and stay there until the next adjustment.

Fixed rate mortgages, at least for most of them, are set in another manner but also use a specific index. Currently, the index used for most fixed rate conforming loans is the Universal Mortgage Backed Security, or UMBS. This is the index lenders use when setting fixed mortgage rates scheduled to be sold to either Fannie Mae or Freddie Mac.

Okay, so if most lenders use the same index when setting fixed rates, why are they sometimes different? That can depend upon different factors. Lenders compete for mortgage business in different ways, but they all want to compete based upon a competitive rate. The rate doesn’t always have to be the lowest rate but should be in the ballpark.

Maybe a customer has a long-lasting banking relationship with a bank and also has quite of bit of cash sitting in different checking and savings accounts. That customer might be offered an extremely competitive rate based upon loyalty of the customer as well as the amount of assets the bank holds. The rate in this instance doesn’t have to be the lowest because the borrower is focused more on trust and relationships than the rock-bottom rate.

On the flip side, for mortgage companies that don’t have such an established relationship, rates take on a more serious note. A mortgage company with less media exposure compared to established banks might need to entice a potential borrower with some very competitive mortgage rates. But again, they set their prices on the same set of indices.

Sometimes a mortgage lender has taken an aggressive approach and priced their loans very low and suddenly their pipeline is full. They’re overbooked and overworked. Their marketing campaign is working but now their loan processing times have slowed to a crawl. It’s not unheard of for a mortgage company to raise rates temporarily to turn off the spigot. It happens. Lenders certainly want to make a profit, otherwise the mortgage market would dry up, but they want to be smart about it.

Message me if your thinking about buying a Fort Collins or Loveland home at m.me/EdPowersRealEstate

Ed Powers Real Estate 970-690-3113 ed@EdPowersRealEstate.com www.EdPowersRealEstate.com

House flipping is one business where it pays to find the cheapest ways to transform a living space. Although you never want to cut corners on quality, you can cut your expenses down by focusing on renovating the rooms that really matter. Buyers today often choose homes that they know might need a little fixing up such as the garage. However, they do tend to prefer homes that already have the necessary rooms remodeled so that they can begin enjoying it right away. Focusing on these areas of the house will make it easier to flip it fast once you put it on the market.

Create a Multifunctional Spare Room

Many homes today have a spare room that tends to be slightly smaller than the others. In older homes, this room might have once been used as a sitting room to visit with guests. Newer homes often advertise this room as an office. Since the room is smaller, it is easy to do a fast renovation such as adding a fresh coat of paint. You can also upgrade the windows and add a decorative door that allows it to be used for anything from a home office to a kid’s playroom.

Cook Up a Sale with a Gorgeous Kitchen

Today’s modern open floor plans make it impossible to hide a poorly designed kitchen. In most cases, you can expect that the kitchen will be one of the first things that buyers will ask to see. Even when a kitchen is hidden from public view, buyers want to know that they’ll have a comfortable place to prepare meals and gather with their friends. Kitchen remodeling is a must for any time that you are flipping a house. Upgraded countertops, cabinets and floors go a long way toward getting people interested in your house.

Dazzle Buyers with a Stunning Master Bathroom

The master bathroom falls close to the kitchen when it comes to areas that people notice. Check out the hottest bathroom trends before you plan a remodel, and try to incorporate a few into your plans. Adding double sinks or a soaking tub will have buyers imagining themselves relaxing in the spa-like space at the end of a long, hard day.

There is an art to making money as a house flipper. Learning where to save on costs and when to invest is as simple as understanding the preferences of the average buyer. When you think about it, it just makes sense to spruce up the areas of a house where people spend the most time. Choosing to upgrade a kitchen or bathroom may require a little extra work, but it can pay off by giving you a much higher profit margin in the end.

Message me if your thinking about buying or selling a Fort Collins or Loveland home at m.me/EdPowersRealEstate

Ed Powers Real Estate 970-690-3113 ed@EdPowersRealEstate.com www.EdPowersRealEstate.com