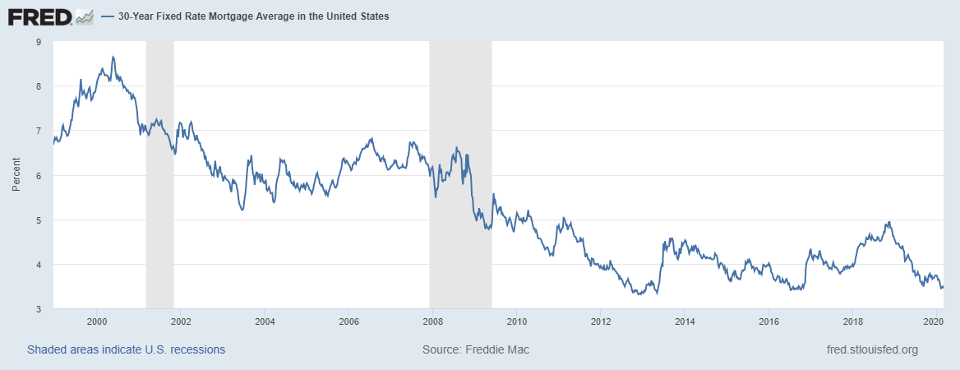

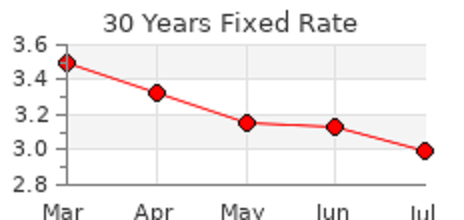

30 Year Mortgage Rates on FHA Loans pushed lower reaching a new low of 2.79%, according to Bankrate, independent, advertising-supported publisher and comparison service, that tracks mortgages. Congressional gridlock over the next fiscal relief could drive rates even lower.

The limited supply of homes on the market continue to cause an obstacle to buyers looking to own a home. Credit tightening is also putting a squeeze on buyers to qualify for these record low rates.

Message me if your thinking about buying or selling a Fort Collins or Loveland home at m.me/EdPowersRealEstate

Ed Powers Real Estate 970-690-3113 ed@EdPowersRealEstate.com www.EdPowersRealEstate.com

Scoffers label it, ‘panic-moving.’ Others call it common sense. Wherever you stand, there is little doubt that, as the pandemic continues to surge, the flight of families from city to suburbs is picking up steam across the nation.

“Young New York couples typically put off a move to the suburbs until after the birth of their second child,” said Elizabeth Nunan, president of Houlihan Lawrence, a leading New York residential brokerage. “It gives them time to save some money and enjoy the perks of city living until the need for space and the cost of childcare make the family-friendly suburbs a better choice.”

But circumstances have flipped the concept on its ear.

“Living in the epicenter of the coronavirus pandemic left most New Yorkers justifiably fearful,” Nunan said. “Theaters and restaurants have all but shut down and, perhaps most important of all, thousands of parents now working from home see that as a continuing possibility at least part of the time.”

For many, Nunan observed, the idea of trading crowds and traffic for a safe space with an outdoor garden quickly grew in appeal – and the perfect storm of changing priorities, professional opportunity, and low interest rates makes it sensible to move up the timeline.

A move to the suburbs is costly.

“The entry price point for a single-family home in Westchester, Greenwich, and similar areas within easy reach of the city is close to $2 million,” Nunan said, “and yet the search for such homes is up some 60 percent over this time last year because, in the age of coronavirus, no one wants to share an elevator or other facilities in a less expensive condo or co-op.”

And the market is hugely competitive.

“It’s definitely a seller’s market,” said Nunan. “Couples are draining their savings, dipping into retirement, getting help from their parents, or pulling cash out of the stock market. Some are making all-cash offers to help them prevail in a multiple-bid situation.”

Atlanta Realtor Debbie Sonenshein, a luxury home specialist with Coldwell Banker, sees a similar dynamic.

“The market revved up fast here in Atlanta,” she said, “where local buyers are competing with buyers flooding in from out of state for upscale homes in the Atlanta suburbs, where a good-sized property with a pool and maybe a view is less costly than in other areas.”

With inventory low, Sonenshein said she and her team are selling new-on-market, single-family homes in good condition for somewhere between $1.65 million and $4 million depending on size, location and features.

“Many of my buyers are in health-related fields,” she said, “young doctors, nurses, people in medical product manufacturing or technology who want to move their families away from cities and hospitals into safer spaces. Others just want to be able to grow tomatoes and bake bread with their kids in a cleaner, greener environment.”

The team frequently makes use of 3D home tours and other visual technologies, Sonenshein added, to help clients narrow their choice, greatly reducing the need for in-home showings.

“We have far fewer homes than we have enthusiastic buyers,” she said. “In-person showings are for serious buyers only, and you’d better be prepared to move.”

Perceptions can vary about where the suburbs begin and end.

“People in San Francisco see Oakland as a suburb, while people in Oakland are swarming into the East Bay or even up to mountain vacation areas like Lake Tahoe,” said Linnette Edwards, founder and associate broker of Abio Properties in northern California. “With inventory tight and interest rates low, buyers are literally coming out of the woodwork, including many young buyers tired of living and working, and even home-schooling, in their 800 square-foot apartments.”

Bidding wars are common, she said, with as many as 15 offers on a single-family residence not at all unusual.

“Young buyers, especially, who can work from home and aren’t tied to their employer’s location, are scrambling to find smaller detached homes with enough yard space to add on office space or an extra bedroom,” she said.

“Prices are ticking up a bit in most areas because of the high demand,” Edwards said. “But it’s still possible to find an entry-level homes for well under $1 million in parts of Oakland and in some East Bay cities, and that is driving demand.”

One local lender, she said, pre-approved 268 borrowers for home purchases in June – an all-time record for the company, up more than 100 percent from last June, when they pre-approved 124 buyers.

“The biggest problem we have is tight inventory,” Edwards said, “although sellers are slowly coming back into the market as they realize the value of their properties.”

Values are changing as people in the age of pandemic re-evaluate what is important to them, said Edwards, who recently purchased a second-home getaway for her own family.

“Watching with your child as a 10-year old African spurred tortoise crosses the road can be the highlight of your day,” she said.

Message me if your thinking about buying or selling a Fort Collins or Loveland home at m.me/EdPowersRealEstate

Ed Powers Real Estate 970-690-3113 ed@EdPowersRealEstate.com www.EdPowersRealEstate.com

For many first-time buyers, a Federal Housing Administration (FHA) loan is the prudent—and often the only—choice for a mortgage. With the flexible credit and low down payment requirements, an FHA loan makes it easier to qualify than almost any loan out there.

However, the ongoing private mortgage insurance (PMI) you have to pay when you have an FHA loan makes your monthly payments more expensive. And, unlike a conventional loan, which allows you to remove your PMI at a certain point, you can never get rid of it with an FHA loan—even when you have tons of equity in your home. So, with rates at historic lows, should you refi out of your FHA loan to a conventional loan? We’re looking at the pros and cons.

Pro: You can get rid of private mortgage insurance (PMI)

“FHA loans require certain provisions which sometimes place a heavy burden on a homeowner’s budget, often in the form of premiums paid for mortgage insurance,” said PennyMac.

That mortgage insurance on an FHA loan ranges from .45–1.05% of your home loan amount every year. On a $285,000 home, “families could be spending more like $3,420 per year on the insurance,” said Investopedia. “That’s as much as a small car payment!”

That money is literally insurance for the lender in case you default on your loan. And, unfortunately, they continue to collect that insurance regardless of how far you pay down your mortgage balance or how much your home appreciates.

“To stop paying PMI on an FHA loan you will need to refinance into a conventional mortgage,” said The Lenders Network.

The solution: refinance to a conventional loan. Assuming you have enough equity in your home, you won’t have to pay mortgage insurance on the new loan. Combined with a lower rate, your monthly payment will drop. “If you have paid down the loan to 78% of the value of the home you can refinance into a conventional mortgage without having to pay PMI.”

Pro: Mortgage insurance for conventional loans may be less expensive

If you refi to a conventional loan and still have to pay mortgage insurance because you don’t yet have enough equity in your home, you may be able to benefit from the lower payments.

“The mortgage insurance fee on a conventional loan is lower than it is with FHA. FHA MIP rates are 0.80% – 1.00%,” said The Lenders Network. “Many conventional mortgages have an annual PMI fee of 0.50%. On a $200,000 home that is savings of almost $80 per month. While it is not a huge savings, the PMI will drop off once the LTV reaches 78%. After dropping PMI, the savings is almost $2,000 per year. You can generally refinance out of FHA into a conventional mortgage after 6 months.”

Cons

With any refi, you’re going to pay closing costs. When you’re refinancing out of an FHA loan into a conventional loan, you can count on those costs ranging from about 1.5% to as much as 3%. So, on a $300,000 mortgage, you’re looking at about $9,000. There may be a few out-of-pocket costs involved in the process; Typically, you’ll be responsible for paying for an appraisal. The rest of the closing costs will come from your equity.

When you’re trying to decide whether or not to refinance, look at the cost to you, and determine how long it will take to recoup the money with your lower payment. If you won’t break even for seven years and you’re planning on moving in three, perhaps it’s time to reconsider whether you should refinance at all.

Message me if your thinking about buying or selling a Fort Collins or Loveland home at m.me/EdPowersRealEstate

Ed Powers Real Estate 970-690-3113 ed@EdPowersRealEstate.com www.EdPowersRealEstate.com

People are spending a lot more time at home. Whether it’s because of a stay-at-home edict or just choosing to work remotely instead of heading toward the office, many are choosing the stay-at-home model and some employers have found the stay-home can be an option for the employee going forward. And spending more time at home might also lead to thinking of a few household projects. Is the kitchen looking a little dated after all? How about some new countertops and upgraded appliances? Is the living room carpet looking a bit threadbare? If so, you’ll need to decide how to pay for those improvements.

The obvious way is to pay cash. It’s quick, interest-free and you can tap into a checking or savings account pretty much anytime you need it. You get a bid, decide whether or not to move forward and write a check. On the flip-side however, pulling money out of an account can put a dent in the balance and in any interest-bearing account, money out no longer pays interest. The bigger the project, the more that’s pulled out. And, once those funds are used to upgrade the kitchen, the asset is no longer liquid, it’s in the cabinets, appliances and flooring.

You can get a home improvement loan to pay for a remodel. With a home improvement loan, your loan goes directly toward the improvements. Depending upon the size of the home improvement loan, the funds might be delivered straight to your bank account at your settlement or if you have a larger project in mind, the bank might deliver the funds in stages as the work is completed.

Say for example you’d like to add on a third bedroom instead of selling your home and buying an existing three bedroom house. This would be considered a major remodel while at the same time increasing the value of your home by adding a third bedroom. This entails hiring an architect and a builder and paying for inspections and final appraisal as part of the process. With such a loan, it is phased in like most any other construction loan. The bank reviews your plans and specs, comes to an appraised value based upon what the final three bedroom project would be worth once complete. When the third bedroom is added on and finished out, one final inspection is performed to confirm completion. At the end of the project, the construction loan becomes due and a permanent mortgage is needed to replace the temporary construction funds.

A home equity loan can also be a solution. A home equity loan is a loan taken out with some of the equity in your home as collateral. There are two basic types of equity loans, a standard equity loan and a home equity line of credit, or HELOC. A standard equity loan is issued as a lump sum payment. a HELOC acts much like a credit card. You’re issued a line of credit based upon the as-completed value. If you want to pull out $10,000 for new appliances, you can do so but you also have the option of paying some or all of that $10,000 back based upon the terms of the loan, freeing up the equity to be used once again at some point in the future.

Another option is to utilize a cash-out refinance. During the process of refinancing an existing loan, homeowners may elect to pull out a little extra after paying off the outstanding principal balance and closing costs. If the loan balance is $200,000 and closing costs are $3,000, the new loan could also include some extra money in the bank account by tapping into the available equity in the home. However, exploring a cash-out refinance should only make sense if a non-cash out refinance lowers the interest rate on a low, changing loan terms, avoiding a balloon payment on its own, then pulling a little extra out in the form of cash might be an option for you.

All of these financing options have their advantages. Your loan officer can break down all the options, compare monthly payments, costs, etc. and help you choose the right financing tool for your individual project.

Message me if your thinking about buying or selling a Fort Collins or Loveland home at m.me/EdPowersRealEstate

Ed Powers Real Estate 970-690-3113 ed@EdPowersRealEstate.com www.EdPowersRealEstate.com

Despite the ongoing coronavirus pandemic, the real estate market must go on. Homeowners still need to sell, house-hunters still need to buy, and real estate agents still need to make a living. But the typical home selling process involves frequent contact with strangers—which is not recommended during this time of social distancing.

By now, you’re probably getting pretty good at making adjustments in your everyday life to protect the health and safety of yourself and those around you. Along the same lines, there are steps you can take to show your home to potential buyers without risking your health or hurting your chances of a sale. Here are some tips to prepare your home for sale in the coronavirus era!

Get Help with Staging

According to The Mortgage Reports, staged homes sell an average of 73% faster than non-staged homes. Staging involves eliminating clutter, incorporating decorative elements, and adjusting the layout of your furniture to improve the flow of your home. The overall goal is to make your home appear bigger, brighter, and more inviting to potential buyers. Fortunately, some staging steps are easy to tackle on your own, such as cleaning, decluttering, and depersonalizing. These steps will help buyers picture themselves living in your home instead of feeling like intruders in someone else’s space.

When it comes to décor, however, it’s best to hire a professional. An interior designer can help you stage your home to effectively show off key aesthetic elements as well as the features that make your space functional. You can easily find freelance interior designers on job boards like Upwork. To keep yourself and your designer safe, make sure they have adopted special procedures to conform with CDC recommendations for COVID-19.

Don’t Neglect Your Curb Appeal

Don’t let your home preparations stop at your front door! Even if buyers aren’t visiting your home in person, they will still want to see your home exterior. In fact, a picture of your home exterior will likely serve as the bait that draws potential buyers to your online listing. Don’t neglect your curb appeal!

Tool Review Lab recommends several ways to boost your curb appeal—even if you’re on a tight budget. For example, you could power wash your front porch and siding, install a new mailbox, hang modern house numbers, and do some basic lawn maintenance.

When it comes to your front yard, make sure your lawn is lush, freshly mowed, and free of weeds and dead spots. Consider planting new flowers and remember to weed and mulch the beds to keep everything looking neat. You may even want to hire a professional to give the trees and shrubs around your yard a good trim.

Consider Safer Showing Alternatives

While it’s clear that hosting an open house is off the table, you may also want to limit in-person showings. Offer your buyers no-contact alternatives! Shoot a video walkthrough of your home and upload it to your online listing so buyers can tour your home virtually. You could even schedule live video-chat showings with interested buyers so they can ask questions about your home or request specific shots of rooms or features.

Since buyers will form a first impression of your home based on your listing, make sure it does your home justice. Write a strong listing title, include a detailed and exciting description, and post plenty of high-quality photos. A great real estate agent can help you craft your listing so that it properly showcases your home’s best features. Your real estate agent can also help you navigate virtual showings! Take the time to find a professional who is well-versed in using online tools to connect with buyers.

Selling a home in the age of the coronavirus is bound to be a bit of a challenge. Thankfully, the real estate industry has been quick to adopt virtual alternatives to open houses and buyers are happy to continue their housing hunt online. With some special attention to staging and a solid virtual presence, you’ll have no problem closing a sale during the pandemic!

Message me if your thinking about buying or selling a Fort Collins or Loveland home at m.me/EdPowersRealEstate

Ed Powers Real Estate 970-690-3113 ed@EdPowersRealEstate.com www.EdPowersRealEstate.com