Children around the U.S. are learning virtually this school year. Some districts are entirely virtual for the time being. Others are doing a hybrid approach combining virtual and in-person learning. Parents are wondering how they can facilitate the best possible experience for their kids when they’re learning virtually. A lot of that has to do with creating a good environment that’s conducive to learning. Choose a Space Separate From Living Areas. One of the most important things to keep in mind when creating a learning space is that it needs to be quiet and separate from the main living and traffic areas of the home. You want your kids to not

to not only be able to focus but also to be able to separate the time they’re learning from the time they’re doing other things. Transforming a guestroom can CONTINUED >>>

There are a lot of reasons you might feel like it’s time to downsize and move into a smaller home. If you’re now an empty-nester, that’s one good reason. Even families who still have children at home often opt to downsize to save money on their mortgage and to have less upkeep and maintenance. If you spend all of your free time maintaining a larger home than what you need, you have less time to enjoy your life. When you downsize to a smaller home, you can declutter and enjoy lower utility bills. Living in a smaller home requires you to think about your priorities and get rid of things that aren’t CONTINUED >>>

With interest rates flirting again with historic lows over the past couple of months, many are looking to invest in real estate. Rates are low and as such the situation offers the opportunity for monthly cash flow as well as long term appreciation. If you’re looking to expand your portfolio and get beyond stocks, bonds and mutual funds, adding real estate might be an option. When financing a rental, there are some things you need to know about before moving much further along. The first is how much cash you’ll need at the closing table. Conventional loan programs ask for a minimum of 20% for a down payment and can offer slightly better terms with a 25% down payment. Owner-occupied loan programs can ask for a minimum down payment of 5%, with certain targeted areas qualifying for a 3% down option. One of the drivers behind the difference in down payment requirements for the same type of property is private mortgage insurance, or PMI. Down payments CONTINUED >>>

Being a freelancer, contract worker, gig worker, or anyone self-employed is more common and popular than ever right now. There are downsides, such as the lack of benefits like health insurance. At the same time, there are more upsides for many professionals who choose to work this way. Upsides include freedom and flexibility to make your own schedule, unlimited earning potential, and the ability to have the work-life balance that allows you to create your own lifestyle. There is an issue that can arise if you’re a freelancer or contractor, though. How do you get a mortgage? When you apply for a mortgage as a traditional employee, you’ll probably show your proof of income through your job, but it can be a bit trickier if you don’t have a traditional employer. You’re also going to face more scrutiny from lenders. Keep Up with Relevant Documents Over the years, it’s easy to be disorganized as far as how you keep up with your earnings and expenditures, but come time to apply for a mortgage CONTINUED >>>

Read about the events shaping the Real Estate market today, find current interest rates, or browse the extensive library of advice and how-to articles written by some of the top experts in Real Estate. Updated each weekday.

Read about the events shaping the Real Estate market today, find current interest rates, or browse the extensive library of advice and how-to articles written by some of the top experts in Real Estate. Updated each weekday.

“What do I need to know about the plumbing?” The answer can be rather long and rather complex, but in the simplest of terms, the plumbing of a home consists of two major parts:

• Supply System – the plumbing that brings fresh water into the home, a connection of sealed pipe sections and valves under pressure, which are intended to bring a continuous flow upon demand

• Drainage System – the plumbing that safely removes used water and waste products from within the home through a series of vented pipe sections which flow downward to allow discharge via gravity

Well, that is about as simple as the explanation gets, water in, and waste out. But there is much more to the story, such as the types of piping used, “are the pipes made of plastic, copper, or galvanized steel”?

And, “what types of connectors are used, brass fittings, soldered connectors, or adhesive materials?” And then, “what other types of fixtures or accessories are found within the system; are there well pumps, storage tanks, pressure regulators, treatment systems, water heaters, and so on?”

And, “what types of traps or clean-outs are provided for the toilets, sinks, and tub/showers”? Wow, so many things to cover, and so many locations for possible leaks. After all, plumbing systems in good service are those that deliver the inbound potable water upon demand, and then take the contaminated waste water outbound, and without any leakage along the way!

Let’s talk about the supply piping first. Prior to the early 1960’s, most homes built in the last century used inbound water pipes made of galvanized steel, galvanizing being a process of coating raw steel pipes through a corrosion resistant chemical process. Galvanizing worked well, but typically this coating material began to breakdown over time, which then left the steel piping exposed to water which in turn began the process of decay.

Usually galvanized piping had a life expectancy of approximately 40 years, maybe a bit longer depending upon their use, maintenance, or original installation methods. If the home you are purchasing has galvanized piping, it may be getting up in age and therefore this system may need to be replaced at some future point in time. Signs of corrosion or visible signs of rust detected during an inspection may suggest that the system has areas of decay, and that further evaluation may be advised.

Some other older supply systems to watch out for are various forms of flexible plastics. Only a few types of plastic piping are recommended for use within supply systems by the International Residential Code and the Uniform Plumbing Code, and these uses are very specific in nature. If you have any plastic supply piping, this should be given special attention as these are not common, and some plastic systems have been prone to have problems. Expert advice should be sought under these conditions.

Now fast forward in time just a bit. After the 1960’s construction methods began using copper piping almost exclusively. With the exception of some weaker versions of the first copper pipes (there are various grades K,L,M), extruded copper plumbing has become the gold standard. Almost all supply piping installed today in residential construction is made of copper. This type of material is largely resistant to corrosion from water, is easier to install and/or repair than steel products, and in most cases copper has become the most cost effective material overall.

The only concerns with copper piping are with respect to its softer material which is subject to puncture if struck, by a nail for example, or it may rupture if bent by accident or not supported properly. Copper piping is also subject to galvanic oxidization if connected to galvanized steel piping. Meaning that if a steel connector or section of galvanized steel pipe is attached to a copper pipe, a corrosive reaction develops slowly, usually at the point where the two sections meet.

And remember, corrosion then ultimately leads to decay and leakage. If you have copper piping, keep the entire system made of copper and all will be fine (brass fittings may also be used with copper piping as an alternative material). There are special dielectric connectors that may also be used if a steel pipe is to be connected to a copper pipe.

Okay, we are getting a bit beyond the simple explanations we promised. Just remember:

• copper = good, this is the most common material used today

• galvanized steel = fine, but regular inspection advised due to older materials

• plastic = okay, but for specific uses only in supply systems

Now before we leave the supply piping discussion we need to revisit “what does corrosion on piping really mean?” Corrosion is a process whereby external materials or very small amounts of water are making their way to the surface. Put another way, this could mean that the threads or connections where two sections of piping come together are not completely sealed tight, and therefore tiny amounts of water can get through any small gaps, thus making their way to the outside of the connection. Remember these supply water pipes are under pressure, so any weakness will give water a place to escape.

Now in this example of threaded piping, if the threads are not damaged, cleaning them with a wire brush and then adding Teflon-tape or other piping compounds to the threads might be all that is required to stop further corrosion or leakage. Repairs are not always this simple, but the point here is that corrosion is the first indication that something is not right, so any mention of corrosion on pipes/connectors or fixtures should be taken seriously as this is the plumbing systems “early warning” that repairs are needed. Left unattended, corrosion becomes a leak, and although this process may take months or weeks before a leak appears, it WILL lead to a leak at some point in time. So like most things, the sooner the problem is addressed the better!

Now let us talk about the waste or outbound drainage plumbing systems. Before the 1960s most residential applications were of clay tiles or cast iron piping (and a few less common uses of lead, brass, etc). Clay tiles didn’t last very long, only 25-40 years typically, so any clay piping still in use would be suspect to cracks and leakage. Cast iron on the other hand could last up to 80-100 years by some estimates, but also noting that there have been reports of cast piping failures as early as 40-60 years of use.

Since most of a home’s waste plumbing may be buried under a floor/slab or within the soil, it is hard to really know the true condition of the entire waste system. That being said, an inspection of the visible sections is a great placed to start, and this visual inspection can provide an indication of how the rest of the system may be functioning. Additionally, in the case of concealed areas within the soil for example, visual inspections for wet areas can also be an indication of an active leak.

Or if the water flow out from toilets/tub/showers appears to be slower than usual, this could be an indication of a break or blockages within the waste lines. If problems such as these are evident, further evaluation by a licensed plumber might be recommended, whereby these professionals could send a camera scope through the waste lines to visually inspect then from the inside out. As previously stated, the aim of any initial inspection is to detect possible warning signs, to give a general assessments, and then to recommend next steps accordingly.

If we look beyond early waste systems of clay tiles and cast iron, we move to today’s almost exclusive use of ABS plastic piping (Acrylonitrile-Butadiene-Styrene schedule 40, typically black in color). Okay, that was a mouthful, but one word to remember: “Plastics.”

Unlike supply systems, for waste systems the use of plastics has appeared to have been a huge success! ABS plastic is smooth (unlike the sand-paper texture of cast iron) so clogs due paper getting caught inside the waste lines have been drastically reduced. Plastic is also rigid, meaning that unlike clay pipes that crack if struck or squeezed by tree roots, plastic piping is more likely to withstand these external forces. And did we mention that installing or repairing ABS plastic waste lines is much easier and less costly than the other materials.

Now no discussion of waste systems would be complete without a brief mention of the many connections and fixtures used. Remember that every connecting point is an opportunity for leaks. Every toilet, sink, shower, and water-using appliance should be thoroughly checked. This starts with a visual inspection to determine if the parts were assembled properly. Then further assessments are taken to look for corrosion, stains, and leaks … these steps all begin the process of “early warning” and detection! And then of course, running water through the system can be a final measure of the waste system’s current condition.

A standard inspection process may look at literally hundreds of connection points in an average home. And in addition to determining the types of materials installed, the inspection process will try to weed-out any potential problem areas. Remember, no matter what type of system you have, the key is to keep a watch out for the signs of corrosion or leakage! Plumbing system problems can be serious and costly concerns, but the home inspection can help make the process of detection and analysis a little less of a concern.

And that completes today’s course of Plumbing 101.

Message me if your thinking about buying a Fort Collins or Loveland home at m.me/EdPowersRealEstate

Ed Powers Real Estate 970-690-3113 ed@EdPowersRealEstate.com www.EdPowersRealEstate.com

Starting in March, life as we knew it started shifting for most of us because of the coronavirus pandemic. Non-essential businesses were shuttered, schools were closed, and we started spending a lot more time at home.

The pandemic is still going on, despite most states being in some phase of their reopening plan, and people are doing more things virtually than ever before.

For example, some employers are saying they’ll keep their employees working remotely for the foreseeable future.

A Changing Real Estate Market?

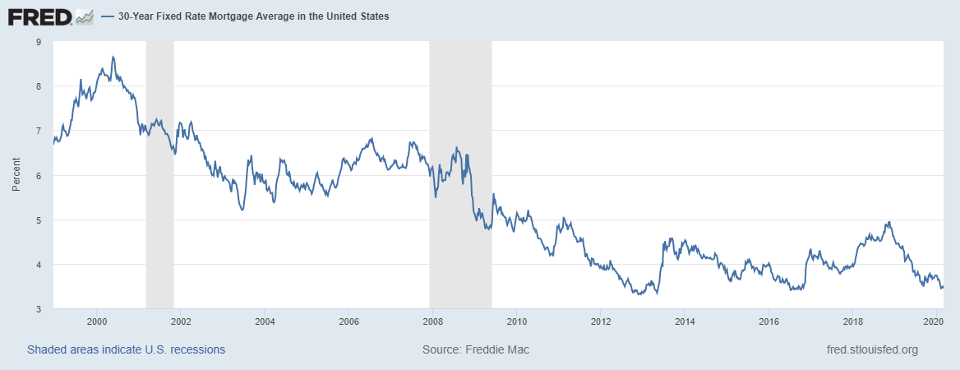

Inevitably, these changes have impacted the real estate market. The market has been surprisingly strong through this, with mortgage rates historically low, but that doesn’t mean buyers and sellers aren’t doing things differently.

The virtual tour is one example. Increasingly homebuyers are going through the entire process online, meaning realtors are showing them homes virtually.

A survey that came out in January, before the pandemic affected America, found that prospective homebuyers preferred to work with agents offering virtual tours. The National Association of Realtors’ 2019 report called “Home Buyer and Seller Generational Trends,” found that 48% of buyers between the ages of 39 and 63 said they found virtual tours very useful as they searched for homes.

The following are things buyers, sellers, and real estate agents should know about virtual home tours.

Agents Can Go in the Home to Do the Tour

The term virtual tour is somewhat generalized, and it can refer to a few different scenarios.

In one scenario, there’s a virtual tour that’s prerecorded, and then anyone can look at it on demand.

There are also instances, particularly now, where real estate agents representing buyers will go into the home and then walk them through it live, but still virtually using something like Zoom or FaceTime.

For some buyers, this represents a better option because their agent can help them understand the nuanced details of the home that they wouldn’t have access to otherwise. If you have a real estate agent who’s doing a tour for you, it’s a much more dynamic experience.

You can ask your agent to show you closets, or provide different angles. You can also ask them to look in the backyard or to examine certain components of the house like the foundation.

What are the Pros of Virtual Tours?

Since we’re still dealing with the effects of the pandemic, one of the perks of virtual tours for buyers is that it provides them with inherent social distancing.

Some people who might be planning a move far from their current location may not even have the option to travel right now, so virtual tours are the only way for them to conduct their search.

It’s also convenient, and there’s a lot to be said for that.

When you take a virtual tour, you don’t want to spend time traveling to the property if it’s something you’re not interested in.

Even if you don’t buy your home completely sight unseen, virtual tours can save you time in the overall process.

Virtual tours can help you get a handle on what you like and don’t like as well.

What Are the Cons of Virtual Tours?

There are downsides to virtual tours. First, you don’t get the full sensory experience of a home. It sounds silly, but homes have a “vibe” and you may feel one way or another about a space when you’re there in person. You don’t feel what the ceiling heights are as an example, or what the finishes feel like.

You’re also not getting a feel for the location if you buy a home without seeing it first. You can ask your real estate agent to provide you with information and perhaps even a virtual tour of the neighborhood, but still, it’s not the same as seeing it for yourself.

Tips for Virtual Tours

If you’re a buyer, there are some things to know going into virtual tours.

First, know what to ask your real estate agent if you’re doing a live tour. For example, remember to ask about the fundamentals like the laundry room, the garage, and the storage spaces. Have your agent show you the roof and the foundation, as well as the less glamorous parts of the house like the water heater and the furnace.

If possible, even if you aren’t going to go to the home, but you live relatively close by, try to drive around and see what you think about the neighborhood.

Finally if at all possible think of virtual tours as one part of your home buying process rather than a complete replacement. They can supplement your experience and save you time, but if you have the chance to go into the home it can help you visualize yourself there.

Message me if your thinking about buying a Fort Collins or Loveland home at m.me/EdPowersRealEstate

Ed Powers Real Estate 970-690-3113 ed@EdPowersRealEstate.com www.EdPowersRealEstate.com

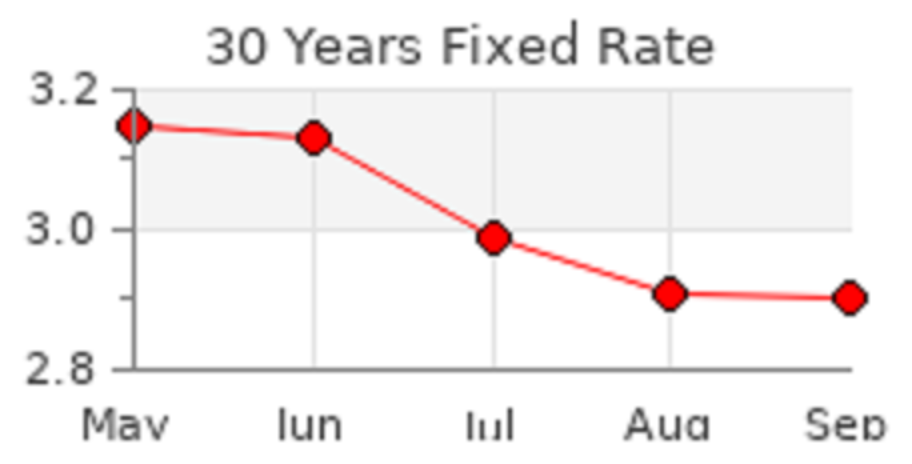

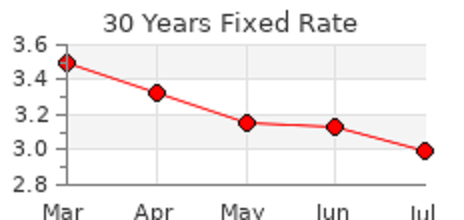

30 Year Mortgage Rates on FHA Loans pushed lower reaching a new low of 2.79%, according to Bankrate, independent, advertising-supported publisher and comparison service, that tracks mortgages. Congressional gridlock over the next fiscal relief could drive rates even lower.

The limited supply of homes on the market continue to cause an obstacle to buyers looking to own a home. Credit tightening is also putting a squeeze on buyers to qualify for these record low rates.

Message me if your thinking about buying or selling a Fort Collins or Loveland home at m.me/EdPowersRealEstate

Ed Powers Real Estate 970-690-3113 ed@EdPowersRealEstate.com www.EdPowersRealEstate.com

Scoffers label it, ‘panic-moving.’ Others call it common sense. Wherever you stand, there is little doubt that, as the pandemic continues to surge, the flight of families from city to suburbs is picking up steam across the nation.

“Young New York couples typically put off a move to the suburbs until after the birth of their second child,” said Elizabeth Nunan, president of Houlihan Lawrence, a leading New York residential brokerage. “It gives them time to save some money and enjoy the perks of city living until the need for space and the cost of childcare make the family-friendly suburbs a better choice.”

But circumstances have flipped the concept on its ear.

“Living in the epicenter of the coronavirus pandemic left most New Yorkers justifiably fearful,” Nunan said. “Theaters and restaurants have all but shut down and, perhaps most important of all, thousands of parents now working from home see that as a continuing possibility at least part of the time.”

For many, Nunan observed, the idea of trading crowds and traffic for a safe space with an outdoor garden quickly grew in appeal – and the perfect storm of changing priorities, professional opportunity, and low interest rates makes it sensible to move up the timeline.

A move to the suburbs is costly.

“The entry price point for a single-family home in Westchester, Greenwich, and similar areas within easy reach of the city is close to $2 million,” Nunan said, “and yet the search for such homes is up some 60 percent over this time last year because, in the age of coronavirus, no one wants to share an elevator or other facilities in a less expensive condo or co-op.”

And the market is hugely competitive.

“It’s definitely a seller’s market,” said Nunan. “Couples are draining their savings, dipping into retirement, getting help from their parents, or pulling cash out of the stock market. Some are making all-cash offers to help them prevail in a multiple-bid situation.”

Atlanta Realtor Debbie Sonenshein, a luxury home specialist with Coldwell Banker, sees a similar dynamic.

“The market revved up fast here in Atlanta,” she said, “where local buyers are competing with buyers flooding in from out of state for upscale homes in the Atlanta suburbs, where a good-sized property with a pool and maybe a view is less costly than in other areas.”

With inventory low, Sonenshein said she and her team are selling new-on-market, single-family homes in good condition for somewhere between $1.65 million and $4 million depending on size, location and features.

“Many of my buyers are in health-related fields,” she said, “young doctors, nurses, people in medical product manufacturing or technology who want to move their families away from cities and hospitals into safer spaces. Others just want to be able to grow tomatoes and bake bread with their kids in a cleaner, greener environment.”

The team frequently makes use of 3D home tours and other visual technologies, Sonenshein added, to help clients narrow their choice, greatly reducing the need for in-home showings.

“We have far fewer homes than we have enthusiastic buyers,” she said. “In-person showings are for serious buyers only, and you’d better be prepared to move.”

Perceptions can vary about where the suburbs begin and end.

“People in San Francisco see Oakland as a suburb, while people in Oakland are swarming into the East Bay or even up to mountain vacation areas like Lake Tahoe,” said Linnette Edwards, founder and associate broker of Abio Properties in northern California. “With inventory tight and interest rates low, buyers are literally coming out of the woodwork, including many young buyers tired of living and working, and even home-schooling, in their 800 square-foot apartments.”

Bidding wars are common, she said, with as many as 15 offers on a single-family residence not at all unusual.

“Young buyers, especially, who can work from home and aren’t tied to their employer’s location, are scrambling to find smaller detached homes with enough yard space to add on office space or an extra bedroom,” she said.

“Prices are ticking up a bit in most areas because of the high demand,” Edwards said. “But it’s still possible to find an entry-level homes for well under $1 million in parts of Oakland and in some East Bay cities, and that is driving demand.”

One local lender, she said, pre-approved 268 borrowers for home purchases in June – an all-time record for the company, up more than 100 percent from last June, when they pre-approved 124 buyers.

“The biggest problem we have is tight inventory,” Edwards said, “although sellers are slowly coming back into the market as they realize the value of their properties.”

Values are changing as people in the age of pandemic re-evaluate what is important to them, said Edwards, who recently purchased a second-home getaway for her own family.

“Watching with your child as a 10-year old African spurred tortoise crosses the road can be the highlight of your day,” she said.

Message me if your thinking about buying or selling a Fort Collins or Loveland home at m.me/EdPowersRealEstate

Ed Powers Real Estate 970-690-3113 ed@EdPowersRealEstate.com www.EdPowersRealEstate.com